When are Home Prices Going to Come Down?

Ever since values took off after COVID, I get some version of this question almost every week. Somebody catches me — out on the Sunrise Mountain trail, in line at the store, a neighbor flagging me down while I'm out in the garden — and they say, "Eydie, when are these prices finally going to come down?" It happened again just this week. So I figured I'd sit down and walk you through it the same way I'd walk one of my buyers through it: slow, honest, and with the homework laid out on the table.

Here's the thing people remember. The last time prices ran up like this, they fell right off a cliff. So it's only natural to brace for the same thing — surely it's coming again, right? We're six years past the start of this run-up now, and a lot of folks are still standing there waiting for the other shoe to drop.

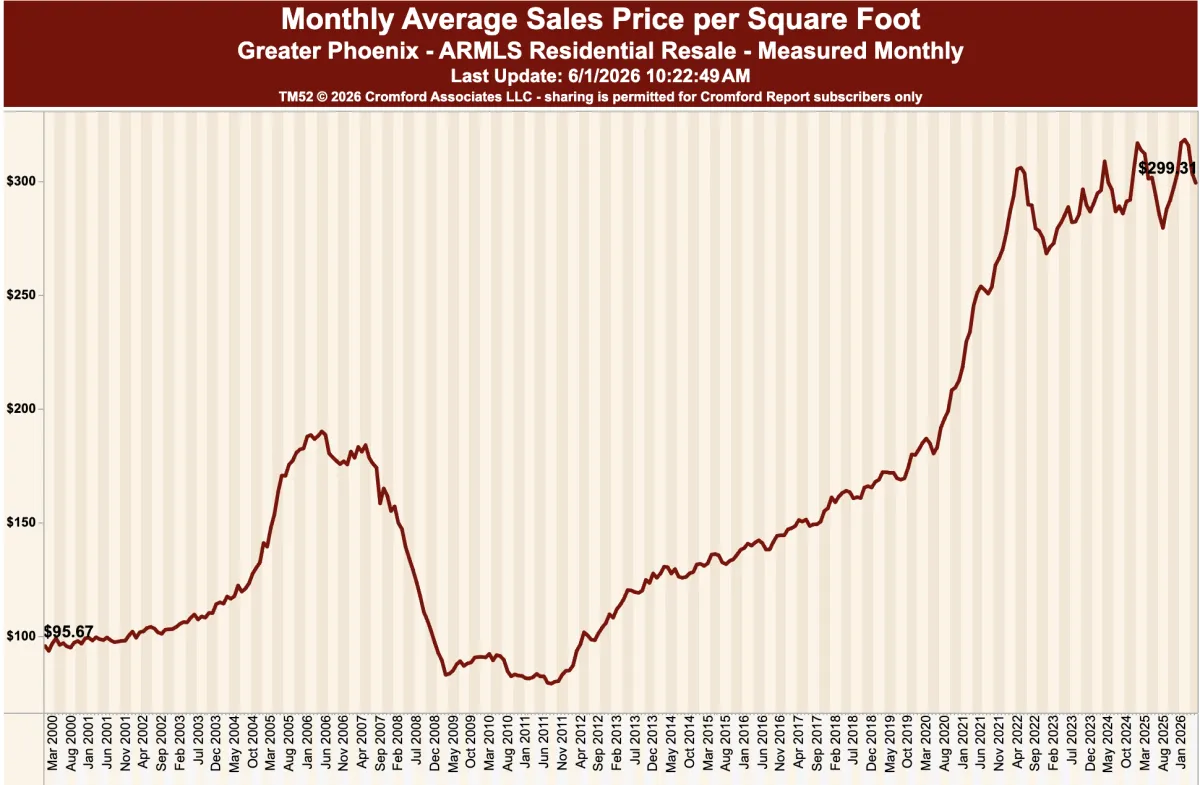

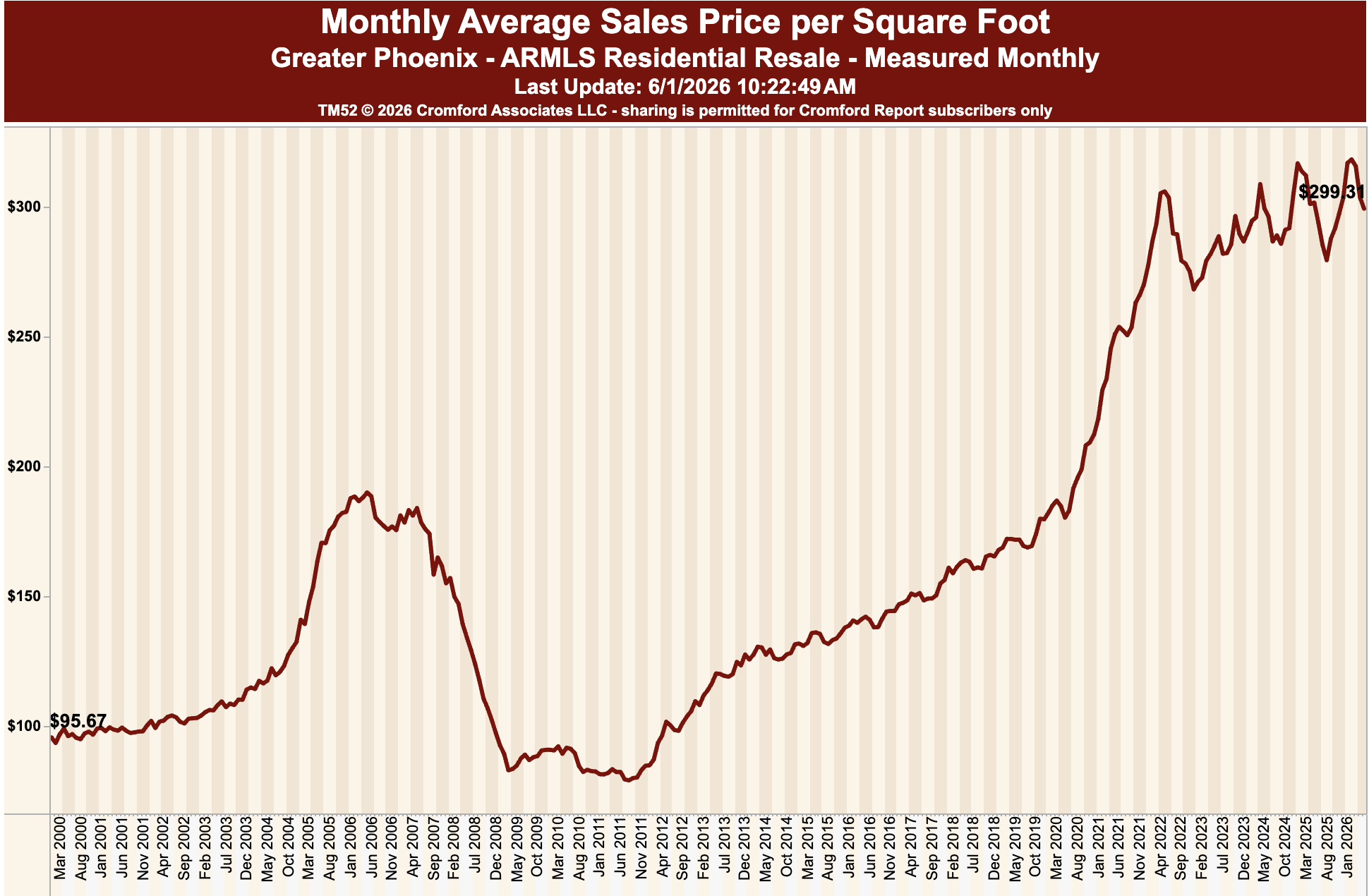

Let me be honest with you, the way I'm always honest with you: I can't tell you the when. Nobody honestly can. I came up as a teacher before I came to real estate, and the one thing teaching drills into you is that you do your homework before you stand up in front of people. So I did mine. And there's one chart that's got me looking at this whole cycle a little differently — I want to show it to you.

First, let's set the outliers aside

A little housekeeping. Let's put the once-in-a-lifetime events off to the side for a minute. As a country we've gotten so used to the big, unexpected stuff that it barely even feels rare anymore — but we still can't predict when those things will hit, or which way they'll shove the market when they do.

Think about it. Hardly anyone saw a global pandemic coming, you know what I'm saying? Let alone one that had the government pumping roughly six trillion dollars into the system. That's $6,000,000,000,000. I bring that number up on purpose, because that flood of money is exactly what makes this particular jump in home values so different from the last one.

Why this cycle isn't like the others

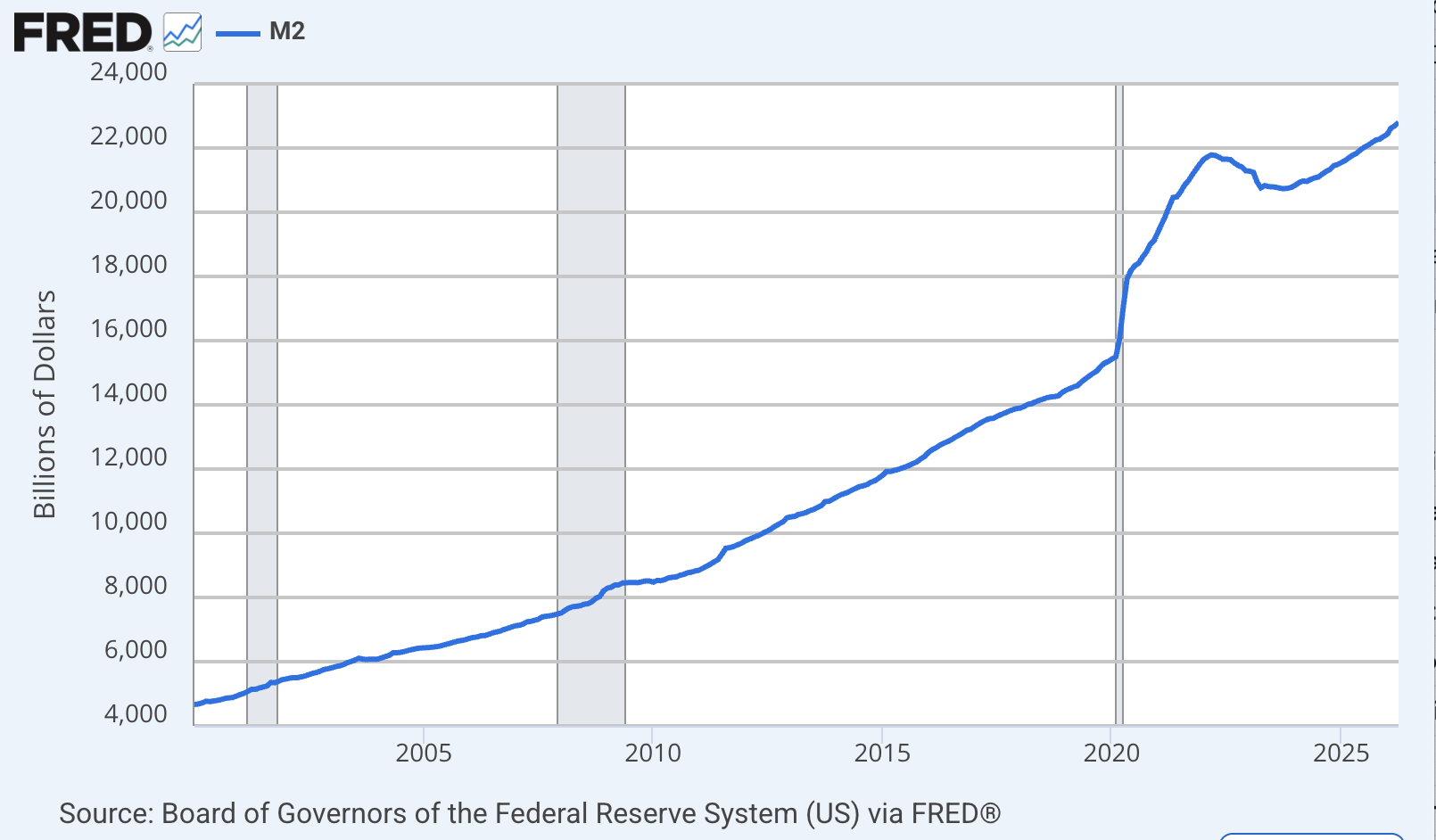

Now, I'll tell you up front — I'm a heart person more than a numbers person. When I'm helping a family, I'm reading them: are they safe, is this the right fit, does it feel right in my soul. But I'm also a paper person. I like to pull the data, print it out, and lay it side by side so it actually makes sense instead of just being an opinion. And every so often I like to pull up the FRED charts. They're a little out of date, and usually too broad to tell you much about a single house — but as a record of where we've been, they're solid. The one I want to look at today is the money chart. The M2.

This one covers the same stretch of time as the home-value run we've all been living through — and that's where it gets interesting.

Back in the 2003-to-2008 run, the money supply barely moved. Home values climbed anyway, on the back of loose credit — and we all know how that ended. It just wasn't built on anything that could hold.

This COVID run-up was a different animal. Values shot up because demand exploded under those low, low, low interest rates — and this time the money supply climbed right alongside them. Almost in lockstep. Both peaked around April of 2022, both eased off afterward, and both have been trending back up since. And it makes me wonder — and I mean wonder, I'm not going to pretend I know — whether that's the reason this jump has held on for more than six years now, when the last one just couldn't.

So — when are they coming down?

What goes up must come down. I believe that, I do. But knowing the when is the whole magic trick, and the honest truth is that timing the market almost perfectly is next to impossible. That's why I keep coming back to this money-supply chart. I'm genuinely curious whether you think it's a fair piece of the puzzle for why values have stayed up. Tell me what you see — I love this stuff, I love learning it right alongside you.

Because here's my hunch. Ask yourself what it would actually take to pull that money supply back down. Whatever the answer is, I'd bet a real dip in home values is standing pretty close to it.

And here's the part I really want you to hear, because it's how I think about everything. Don't try to outsmart the timing. A home isn't a stock you flip — it's something that belongs to you, equity you build, a legacy you pass on to your family. My whole motto in life is make decisions you can live with for the rest of your life. If a home is safe, it's right for your family, and the payment is one you can live with comfortably, the perfect month on a chart was never the thing that mattered. That's the truth I'd tell my own kids. So it's the truth I'll tell you.

Hold the phone — foreclosures are climbing?

Now that one deserves its own conversation. I'll walk you through it in my next article.